Death in service benefit vs life insurance

Death in service is a popular benefit offered by some employers. But who gets death in service benefit and how does it differ to life insurance?

What is life insurance and how does it work?

Life insurance is designed to help protect your family financially by paying out a cash sum if you die during the length of the policy. If you change jobs, or even retire, your life insurance will continue until you die or your policy comes to an end. Cover can be arranged on a joint or single life basis to suit your needs.

You can also opt to put your life insurance in Trust so you have peace of mind knowing that the pay-out will go to the people you intend.

Life insurance is not a savings or investment product and has no cash value unless a valid claim is made.

Life Insurance - Your chosen cash sum could be paid out if you die during the length of the policy. It could be used to help protect the family's lifestyle and everyday living expenses or help to pay the mortgage.

Decreasing Life Insurance - Designed to help protect a repayment mortgage so the amount of cover reduces roughly in line with the way a repayment mortgage decreases. This means your loved ones could continue to live in the family home without worrying about the mortgage.

Critical Illness Cover - can be added to life insurance or decreasing life insurance for an extra cost. It pays out if you’re diagnosed with, or undergo a medical procedure for, one of the specified critical illnesses while your covered, and you survive for 14 days from diagnosis. It could help with child care costs, household bills or to help maintain your standard of living if you're forced to take time off work to recover.

Do I need death in service and life insurance?

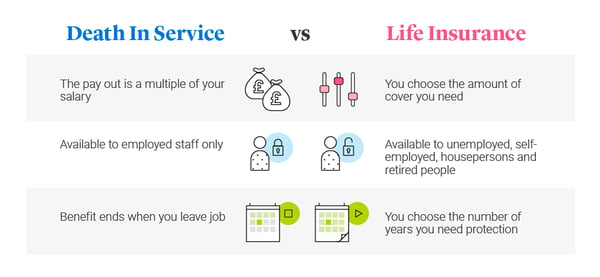

Having death in service benefit is certainly a positive if your employer offers this perk. But you will want to have a long and hard think about whether a multiple of your salary would be enough to support your beneficiaries or loved ones. For example, if you have an outstanding mortgage balance of £300,000, a death in service benefit of £150,000 won’t cover the ongoing costs.

Death in service might seem attractive if you have no intention of leaving your job. But there is no guarantee you will stay in the same role indefinitely. With life insurance you’ll have the security of knowing how long protection lasts. If you keep paying for your policy, you'll have the peace of mind your loved ones could receive a cash sum.

But of course, having some financial protection is better than no protection. Have a think about the protection you would like and contact us if you have any questions about our life insurance products.

Want to learn more about Life Insurance?

Other related articles

Can you have more than one life insurance policy?

The difference between Critical Illness Cover & Income Protection

10 Myths about life insurance debunked